Owner Financing vs. Subject-To: A Houston Seller's Guide

Reviewed by Mark Lee

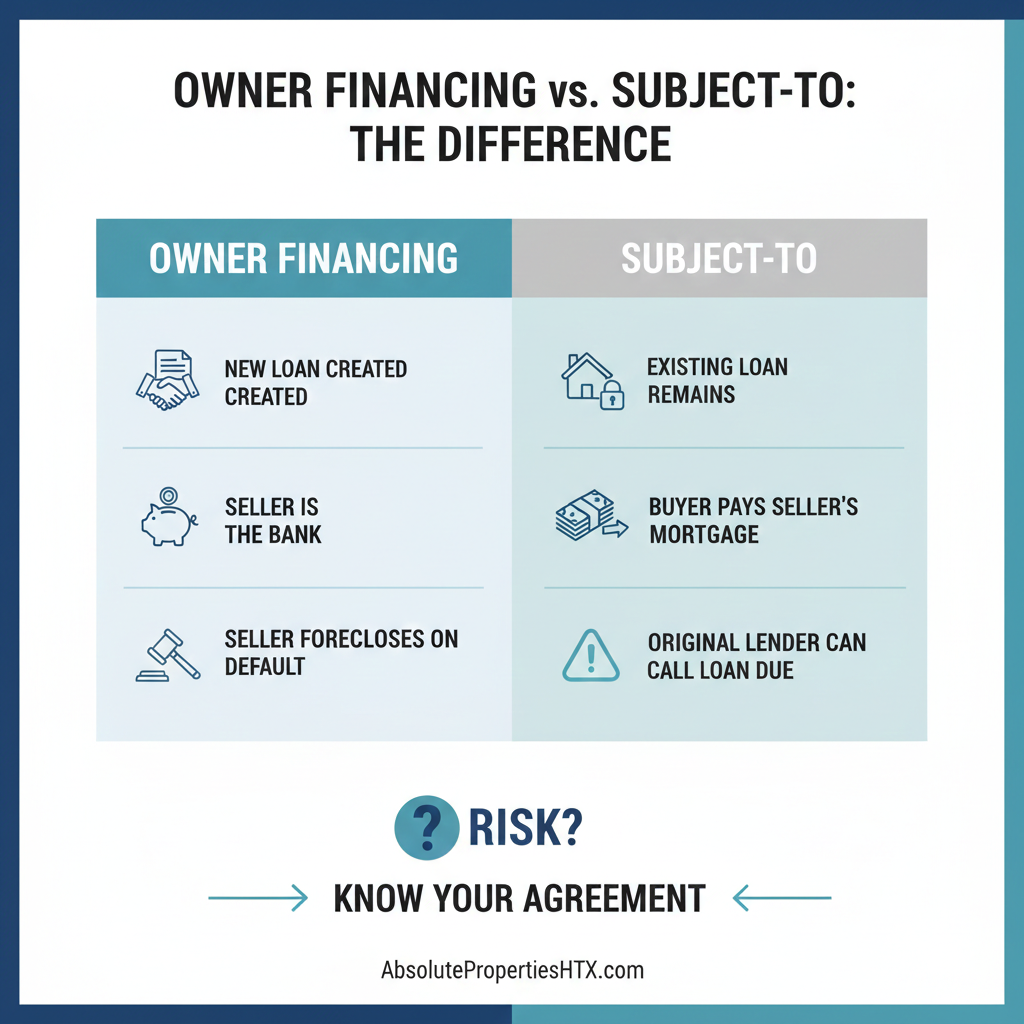

Owner Financing vs. Subject-To: What’s the Difference?

When you’re navigating the Houston real estate market, you quickly realize that the traditional "bank-and-realtor" path isn't the only way to close a deal. In fact, for many homeowners in the Bayou City, creative financing is the secret weapon that allows them to move on with their lives when the conventional route hits a dead end. Two terms that often pop up in these circles are Owner Financing and Subject-To.

While they might sound like legal jargon designed to confuse you, they are actually straightforward tools once you peel back the layers. Whether you are dealing with a property that won't qualify for a traditional loan or you simply want to Sell my house fast Houston without waiting 60 days for a bank's approval, understanding these two methods is essential. They represent two fundamentally different ways of structuring a sale, each with its own set of rewards and risks. Let’s break down the mechanics, the Texas-specific nuances, and which one might be the right "rescue plan" for your situation.

The Mechanics of Owner Financing: You Are the Bank

In a standard real estate transaction, a buyer goes to a bank, gets a mortgage, and uses that money to pay the seller in full. In an Owner Financing (or Seller Financing) scenario, the bank is completely removed from the equation. Instead, the seller extends credit to the buyer to purchase the property.

The buyer doesn't hand over the full purchase price at closing. Instead, they provide a down payment and sign a legal agreement to pay the seller the remaining balance over time, plus interest. You aren't just selling a house; you are creating a private mortgage.

How the Process Works in Texas

Texas has very specific laws governing owner financing, particularly the Texas Property Code. Generally, the process involves a Promissory Note and a Deed of Trust.

The Promissory Note: This is the "I.O.U." It outlines the interest rate, the monthly payment amount, and how long the buyer has to pay you back.

The Deed of Trust: This is your security. It’s the legal document filed with the county (like Harris or Montgomery County) that gives you the right to take the house back if the buyer stops paying.

In Texas, the deed actually transfers to the buyer at closing. They become the owner of record, but your lien stays attached to the property until that final payment is made.

Why Houston Sellers Love Owner Financing

Many sellers choose this route because it expands their pool of potential buyers. You can sell to someone who is self-employed, an immigrant with no US credit history, or someone who just doesn't want to deal with the red tape of a big bank. Because you are providing the financing, you can often negotiate a higher sales price or a higher interest rate than what a bank would offer, turning your equity into a high-yield retirement stream.

Subject-To: Taking Over the Existing Mortgage

If Owner Financing is "creating a new bank," then Subject-To is "taking over an old one." The name is short for "Subject to the existing mortgage."

In a Subject-To deal, the buyer takes over the property, but the seller’s original mortgage stays in place. The buyer becomes the legal owner of the home, but they don't get a new loan. Instead, they simply start making the monthly payments on the seller’s existing mortgage.

How the Deed Transfers

This is where people often get confused. In a Subject-To transaction, the seller signs a deed over to the buyer. The buyer now legally owns the house. However, the mortgage remains in the seller’s name. The buyer is responsible for the payments, but the seller is technically still the one "on the hook" with the bank.

Why Subject-To is a Lifesaver for Sellers

This strategy is most common when a seller has little to no equity or is facing a time-sensitive crisis. If you are behind on payments and facing foreclosure, a Subject-To buyer can catch up your arrears (the "reinstatement" amount) and take over the future payments. This saves your credit from a foreclosure hit and allows you to walk away from the debt immediately.

Key Differences: Debt, Equity, and Liability

The most significant difference between the two boils down to who holds the debt.

Debt Creation: In Owner Financing, you are creating a new debt for the buyer. In Subject-To, the buyer is stepping into your existing debt.

Existing Mortgages: If you still owe a lot of money on your house, Owner Financing is difficult because your bank has a "Due on Sale" clause. Subject-To is specifically designed for properties that still have a mortgage.

The Seller's Credit: With Owner Financing, your credit isn't usually impacted because you aren't the one borrowing money. With Subject-To, the mortgage stays in your name. If the buyer is a day late, it shows up on your credit report. This is why you must only do Subject-To deals with reputable professionals.

Texas "Due on Sale" Realities

Technically, most mortgages have a clause that says the bank can call the loan due if you transfer the deed. In reality, as long as the payments are being made, banks rarely exercise this right because they don't want to go through the hassle of a foreclosure on a performing loan. However, it is a risk that both parties must acknowledge. You can read more about federal regulations regarding these clauses in the Garn-St. Germain Act.

Risks and Rewards for the Houston Homeowner

The Risks of Owner Financing

The biggest risk is the Buyer Default. If the buyer stops paying, you have to go through the legal process of foreclosure. In Texas, this is a "non-judicial" process, which is faster than in many other states, but it still requires an attorney and a few months of time. You get the house back, but you have to deal with the headache of finding a new buyer.

The Risks of Subject-To

The risk here is Non-Payment by the Buyer. Since the loan is in your name, you are vulnerable. If the buyer disappears, your credit score could tank. This is why Subject-To deals usually involve a "Third Party Servicer"—an independent company that collects the money from the buyer and pays the bank directly, giving the seller peace of mind and a paper trail.

Legal Compliance: Dodd-Frank and Texas Property Code

You can't just write these deals on a napkin. Texas is very strict about "Executory Contracts." If you aren't careful, a buyer could sue you to void the entire sale and get all their money back. Using a licensed Texas Residential Mortgage Loan Originator (RMLO) is often a legal requirement to ensure the buyer can actually afford the payments, protecting you from future liability.

Which Path Should You Choose?

Deciding between these two depends entirely on your financial "math" and your goals.

Choose Owner Financing if:

You own the house "free and clear" (no mortgage).

You want a long-term, high-interest monthly income.

You want to maximize the sales price.

You aren't in a rush to get a massive lump sum of cash.

Choose Subject-To if:

You have an existing mortgage with a low interest rate.

You have little to no equity in the home.

You are behind on payments or facing foreclosure.

You need to move immediately and can't wait for a traditional buyer's appraisal.

FAQ: Creative Financing in Texas

Does the bank have to approve a Subject-To deal?

Usually, no. These deals happen "behind the scenes." While the bank has the right to call the loan due if they find out, they rarely do so as long as the money is flowing.

Can I do Owner Financing if I still have a mortgage?

It’s complicated. Doing a "Wrap-Around" mortgage is possible in Texas, but it requires very specific legal disclosures. If your current interest rate is 3% and you charge the buyer 8%, you "wrap" your loan inside theirs and pocket the 5% difference.

How much down payment should I ask for?

In Houston, most professional sellers ask for 10% to 20% down for owner financing. For Subject-To, the "down payment" is often used to pay the seller's moving costs or to catch up on late payments.

Who pays the property taxes?

In both scenarios, the buyer is the new owner, so they are responsible for taxes and insurance. However, as the seller/lender, you should always verify that these are being paid so the county doesn't put a tax lien on your security.

Summary of Options

FeatureOwner FinancingSubject-ToWho is the lender?The SellerThe Seller's Original BankNew Loan Created?YesNo (Existing loan stays)Title Transfers?YesYesBest for...Free & Clear HomesHomes with MortgagesRisk FactorMedium (Foreclosure risk)High (Credit risk)

Your Next Move

Whether you're looking to become the bank and enjoy passive income or you need someone to take over your mortgage so you can start fresh, creative financing offers a way out when the traditional market says "no." The Houston market moves fast, and the legalities can be tricky, so your next step should be a consultation with a professional who understands the Texas Property Code inside and out.

How Absolute Properties Helps Houston Sellers

Absolute Properties makes it easy for Houston homeowners to sell fast - even when facing challenges like financial difficulties, inherited properties, troublesome tenants, or repairs.

If you’re thinking, “I need to sell my house fast in Houston…” We buy houses in Houston in any situation or condition!

As-is, fast cash offers with clear terms

Many closing costs covered; no realtor commissions in most cases

You choose the closing date (as little as 7 days, case-dependent)

Coordination with experienced title company for a compliant sale process

Call or text: (713) 230-8059

Email address: info@absolutepropertieshtx.com

Share your street address and timeline for a free consultation and a straightforward number no pressure.

Helpful Houston Blog Articles

How To Sell Your House in Houston Without Sinking Any More Money Into It

6 Tips For First Time Home Sellers in Houston

Hiring an Agent Vs. A Direct Sale to Absolute Properties When Selling Your House in Houston

Who Pays Closing Costs in Texas

The True Costs of An FSBO Listing for Houston Investors

What To Do With Your Expired Listing in Houston

Also check out our Free Guides & Education & FAQ for more education on how to sell your house for cash quickly to a local home buyer.